By the Fourier theorem, any price curve is a mix of many long-term and short-term cycles. Once in a while a dominant market cycle emerges and can be exploited for trading. In his TASC 5/2026 article, John Ehlers described an algorithm for detecting such dominant cycles, using them to tune a bandpass filter, and creating a profitable trading system. Here’s how to do it.

Ehlers’ Easylanguage code from the TASC article can be directly converted to C for Zorro. ChatGPT does the job in a few seconds. First, the cycle detector:

var MinCorr, Filt;

var AutoTune(vars Data,int Window)

{

Filt = HighPass3(Data,Window);

vars HP = series(Filt);

var Corr[256];

int Lag, J;

for(Lag = 1; Lag <= Window; Lag++)

{

var Sx = 0., Sy = 0.;

var Sxx = 0., Sxy = 0., Syy = 0.;

for(J = 0; J < Window; J++)

{

var X = HP[J];

var Y = HP[Lag + J];

Sx += X; Sy += Y;

Sxx += X*X; Sxy += X*Y; Syy += Y*Y;

}

var Den1 = Window*Sxx - Sx*Sx;

var Den2 = Window*Syy - Sy*Sy;

Corr[Lag] = (Window*Sxy - Sx*Sy) / sqrt(fix0(Den1*Den2));

}

MinCorr = 1.;

var DC = Window;

for(Lag = 1; Lag <= Window; Lag++)

if(Corr[Lag] < MinCorr) {

MinCorr = Corr[Lag];

DC = 2*Lag;

}

vars DCs = series(DC,2);

return DCs[0] = clamp(DC,DCs[1]-2.,DCs[1]+2.);

}

The output of the AutoTune function is supposed to be the dominant price cycle in units of bars. It is then used to set the center frequency of a bandpass filter. Since Zorro has already a bandpass filter in its arsenal, I named Ehlers’ new version BandPass2:

var BandPass2(vars Data, int Period, var Bandwidth)

{

var L1 = cos(2.*PI/Period);

var G1 = cos(Bandwidth*2.*PI/Period);

var S1 = 1./G1 - sqrt(1./(G1*G1) - 1.);

vars BP = series(0,3);

return BP[0] = 0.5*(1.-S1)*(Data[0]-Data[2])

+ L1*(1.+S1)*BP[1] - S1*BP[2];

}

Here’s some code for reproducing Ehlers’ ES chart in the article:

function run()

{

BarPeriod = 1440;

StartDate = 2024;

EndDate = 2025;

asset("ES");

var DC = AutoTune(seriesC(),20);

var BP = BandPass2(seriesC(),DC,0.25);

plot("Zero",0,NEW,BLACK);

plot("BP",BP,LINE,BLUE);

}

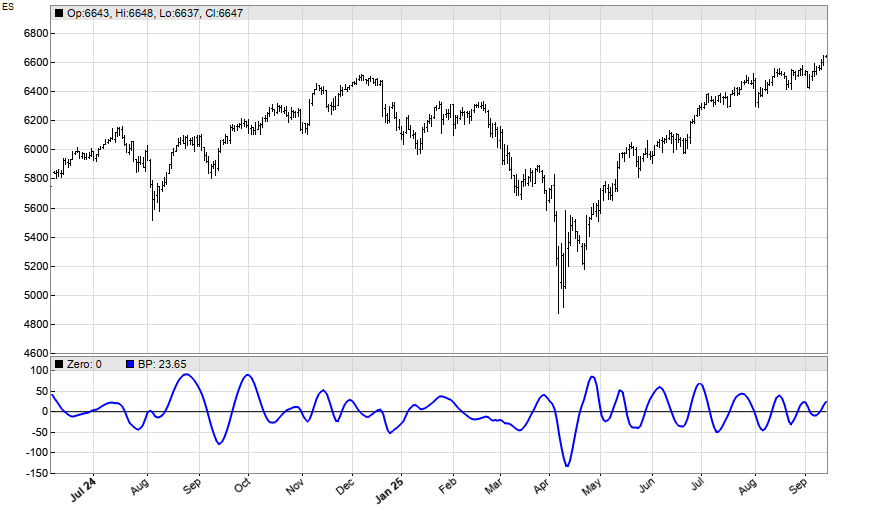

The resulting chart:

How can we use this bandpass output for a trade signal? Ehlers used the zero crossovers of its rate-of-change (ROC). In this way he generated an impressive equity curve in his article, unfortunately with in-sample optimization. For a more realistic result, we’re using walk-forward analysis and reinvest profits by the square root rule:

function run()

{

BarPeriod = 1440;

StartDate = 2010;

EndDate = 2025;

Capital = 100000;

asset("ES");

set(TESTNOW,PARAMETERS);

NumWFOCycles = 10;

int Window = optimize("Window",26,10,30,2);

var BW = optimize("BW",0.22,0.10,0.30,0.01);

var Thresh = -optimize("Thresh",0.22,0.1,0.3,0.01);

var DC = AutoTune(seriesC(),Window);

var BP = BandPass2(seriesC(),DC,BW);

vars ROCs = series(BP-ref(BP,2));

Lots = 0.5*(Capital+sqrt(1.+ProfitTotal/Capital))/MarginCost;

MaxLong = MaxShort = 1;

if(crossOver(ROCs,0) && MinCorr < Thresh)

enterLong();

if(crossUnder(ROCs,0) && MinCorr < Thresh && Filt > 0)

enterShort();

}

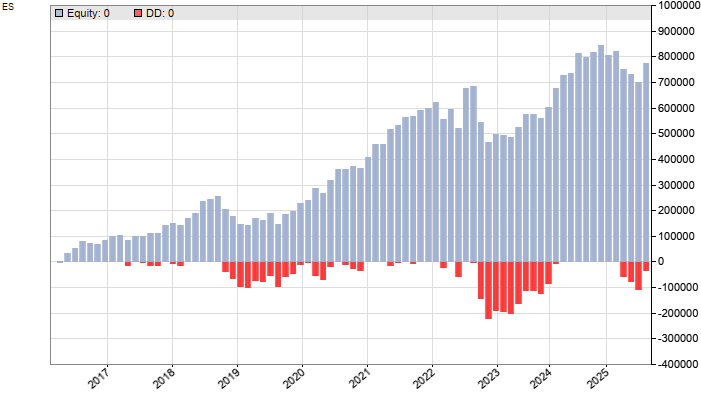

The signals are filtered by a threshold that determines whether we’re in a cyclic market condition or not. The system is not fully symmetrical in long and short positions. Training and testing produced this equity curve:

This curve does not look as impressive as Ehler’s one, but the CAGR is in the 25% area, much better than a buy-and-hold strategy. The code can be downloaded from the 2026 script repository.

One thought on “The AutoTune filter”