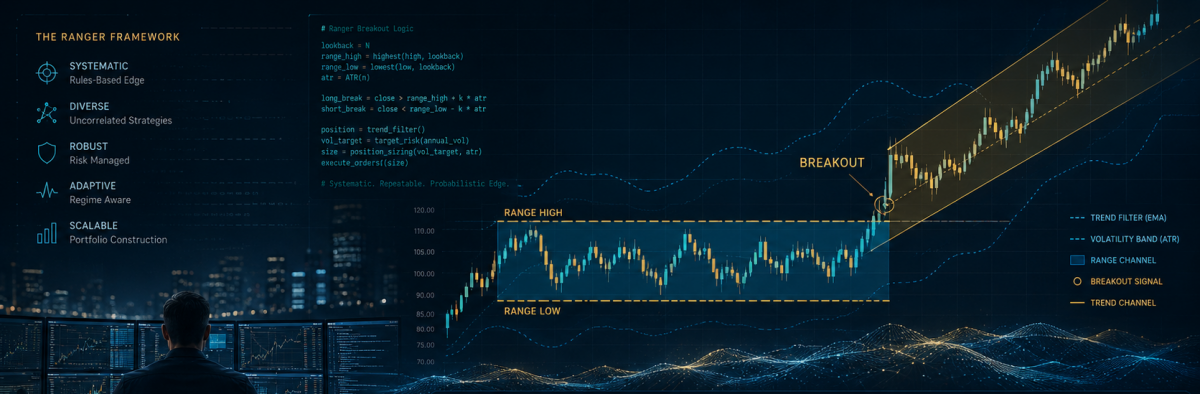

There are traders who became famous due to winning competitions, inventing indicators, managing large funds, or having lucky years. Robert Pardo became known for changing the way trading strategies are optimized and tested. And he gained further fame for the trading systems that he developed over the last 30 years for large investment firms. His latest development, Ranger, produced spectacular returns in the past years, despite the turbulent markets. Is this the one system to rule them all? Continue reading “Evaluating Robert Pardo’s Ranger System”

Category: System Development

The AutoTune filter

By the Fourier theorem, any price curve is a mix of many long-term and short-term cycles. Once in a while a dominant market cycle emerges and can be exploited for trading. In his TASC 5/2026 article, John Ehlers described an algorithm for detecting such dominant cycles, using them to tune a bandpass filter, and creating a profitable trading system. Here’s how to do it.

Build Better Strategies, Part 6: Evaluation

Developing a successful strategy is a process with many steps, described in the Build Better Strategies article series. At some point you have coded a first, raw version of the strategy. At that stage you’re usually experimenting with different functions for market detection or trade signals. The problem: How can you determine which indicator, filter, or machine learning method works best with which markets and which time frames? Manually testing all combinations is very time consuming, close to impossible. Here’s a way to run that process automated with a single mouse click. Continue reading “Build Better Strategies, Part 6: Evaluation”

A Better Stock Rotation System

A stock rotation system is normally a safe haven, compared to other algorithmic systems. There’s no risk of losing all capital, and you can expect small but steady gains. The catch: Most of those systems, and also the ETFs derived from them, do not fare better than the stock index. Many fare even worse. But how can you make sure that your rotation strategy beats the index? There is a way.

Trading the Channel

One of the simplest form of trend trading opens positions when the price crosses its moving average, and closes or reverses them when the price crosses back. In the latest TASC issue, Perry Kaufman suggested an alternative. He is using a linear regression line with an upper and lower band for trend trading. Such a band indicator can be used to trigger long or short positions when the price crosses the upper or lower band, or when it gets close. Continue reading “Trading the Channel”

Ehlers Loops

Price charts normally display price over time. Or in some special cases price over ranges or momentum. In his TASC articles in June and July 2022, John Ehlers proposed a different way of charting. The relation of two parameters, like price over momentum, or price A over price B, is displayed as a 2D curve in a scatter plot. The resulting closed or open loop is supposed to predict the future price development. Of course only if interpreted in the right way.

Why 90% of Backtests Fail

About 9 out of 10 backtests produce wrong or misleading results. This is the number one reason why carefully developed algorithmic trading systems often fail in live trading. Even with out-of-sample data and even with cross-validation or walk-forward analysis, backtest results are often way off to the optimistic side. The majority of trading systems with a positive backtest are in fact unprofitable. In this article I’ll discuss the cause of this phenomenon, and how to fix it. Continue reading “Why 90% of Backtests Fail”

Buy&Hold? No, Buy&Sell!

There’s no doubt that buying and holding index ETFs is a long-term profitable strategy. But it has two problems. It does not reinvest profits, so the capital grows only linearly, not exponentially. And it exposes the capital to the full rollercoaster market risk. A sure way to go out of the market in a downtrend, and invest the profits back in an uptrend would be (almost) priceless. Markos Katsanos promises no less in his Stocks&Commodities July 2021 article. Does this really work? Continue reading “Buy&Hold? No, Buy&Sell!”

More Robust Strategies

The previous article dealt with John Ehlers’ AM and FM demodulating technology for separating signal and noise in price curves. In the S&C June issue he described a practical example. Applying his FM demodulator makes a strategy noticeably more robust – at least with parameter optimization.

The Mechanical Turk

We can see thinking machines taking over more and more human tasks, such as car driving, Go playing, or financial trading. But sometimes it’s the other way around: humans take over jobs supposedly assigned to thinking machines. Such a job is commonly referred to as a Mechanical Turk in reminiscence to Kempelen’s famous chess machine from 1768. In our case, a Mechanical Turk is an automated trading algorithm based on human intelligence. Continue reading “The Mechanical Turk”